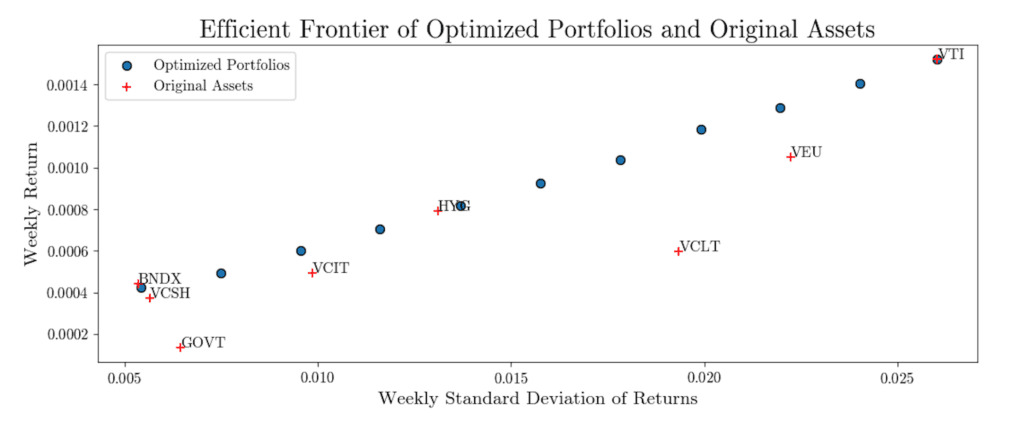

For the past month I’ve been working on a few improvements to the asset allocation model that underpins my portfolio management process at Luther Wealth. I’m really proud of the models currently in place, but I like these new ones even better! I’ve been able to fix some blind spots, and I’ve also been able to avoid some structural problems with one of the equity index funds I have been using. None of these changes are mind-blowing, but I’m proud to work constantly to make small, incremental improvements to my portfolio management process.

For many investors, traditional IRAs are a cornerstone of their retirement strategy, offering the promise of tax-deferred growth and, in some cases, immediate tax benefits. But there’s a quirk in traditional IRA rules that can trip up even the most diligent savers: the treatment of non-deductible contributions.

Failing to track non-deductible contributions to a traditional IRA can set you up for a nasty surprise—double taxation on your distributions in retirement. The good news is that you can easily avoid this problem by keeping good records from the beginning.

Last year, a fintech company called Synpase went bankrupt, affecting bank accounts of over 100,000 clients. This bankruptcy sent shockwaves through the financial technology sector, raising profound concerns among investors, especially those relying on modern fintech custodians. The key problem is the decision by the Federal Deposit Insurance Corporation (FDIC) not to backstop Synapse’s account holders, a move with significant implications well beyond Synapse itself. This decision raises serious questions regarding investor safeguards and custodial protection mechanisms within the broader fintech ecosystem, particularly for robo-advisors and similar services that have garnered sweeping popularity in recent years.

I’ll go ahead and put my main conclusion at the top for this one. Previously, I have been very positive on robo-advisors for certain clients that are willing and able to self-direct investments. Based on the FDIC response and discussion around Synapse, I don’t think any investors should have any money with robo-advisors. Furthermore, I don’t think investors should use any fintech intermediary at all, at least until the FDIC and SIPC catch up to the times.

Your savings should go directly into a real, regulated bank. Your investments should go directly into a real, regulated custodian. Until the FDIC and SIPC say different, if the people you deal with for customer service aren’t the ones getting audited, you are not protected.