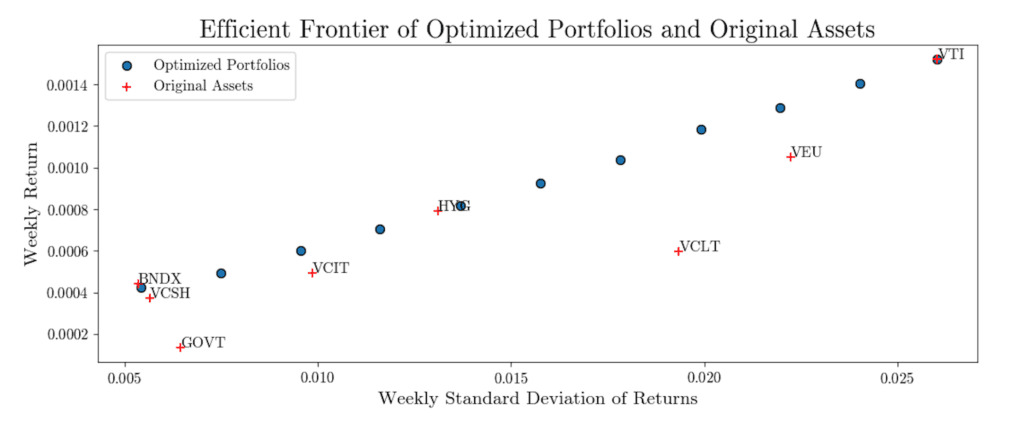

For the past month I’ve been working on a few improvements to the asset allocation model that underpins my portfolio management process at Luther Wealth. I’m really proud of the models currently in place, but I like these new ones even better! I’ve been able to fix some blind spots, and I’ve also been able to avoid some structural problems with one of the equity index funds I have been using. None of these changes are mind-blowing, but I’m proud to work constantly to make small, incremental improvements to my portfolio management process.

For many investors, traditional IRAs are a cornerstone of their retirement strategy, offering the promise of tax-deferred growth and, in some cases, immediate tax benefits. But there’s a quirk in traditional IRA rules that can trip up even the most diligent savers: the treatment of non-deductible contributions.

Failing to track non-deductible contributions to a traditional IRA can set you up for a nasty surprise—double taxation on your distributions in retirement. The good news is that you can easily avoid this problem by keeping good records from the beginning.

Last year, a fintech company called Synpase went bankrupt, affecting bank accounts of over 100,000 clients. This bankruptcy sent shockwaves through the financial technology sector, raising profound concerns among investors, especially those relying on modern fintech custodians. The key problem is the decision by the Federal Deposit Insurance Corporation (FDIC) not to backstop Synapse’s account holders, a move with significant implications well beyond Synapse itself. This decision raises serious questions regarding investor safeguards and custodial protection mechanisms within the broader fintech ecosystem, particularly for robo-advisors and similar services that have garnered sweeping popularity in recent years.

I’ll go ahead and put my main conclusion at the top for this one. Previously, I have been very positive on robo-advisors for certain clients that are willing and able to self-direct investments. Based on the FDIC response and discussion around Synapse, I don’t think any investors should have any money with robo-advisors. Furthermore, I don’t think investors should use any fintech intermediary at all, at least until the FDIC and SIPC catch up to the times.

Your savings should go directly into a real, regulated bank. Your investments should go directly into a real, regulated custodian. Until the FDIC and SIPC say different, if the people you deal with for customer service aren’t the ones getting audited, you are not protected.

I love TreasuryDirect! It’s a free site run by the US Government to allow all citizens to buy US Government debt securities. You can buy several types of savings bonds, and more importantly, you can directly participate in treasury bill, note, and bond auctions. This means that individual investors with as little as $100 can invest on perfectly equal footing with huge institutional investors. They all get exactly the same pricing. It’s amazing! I don’t think there’s any other situation in which an individual can buy a security for such a small amount and get exactly the same terms as CALPERS buying hundreds of millions of securities at the same time. It’s a true egalitarian marvel.

It’s actually slightly dumb for me to even write this article because the service is directly competitive with my core service offering as a fee based financial adviser. The more that my clients or potential clients invest with TreasuryDirect, the less they invest with me, and the less money I make. But I don’t care, it’s such a cool system that I want lots of people to know about it anyway. But before we dive into TreasuryDirect, let’s take a look at how US Treasury auctions work…

Working with a financial advisor can be one of the most important decisions you make for your financial future. A good advisor acts as a trusted guide, helping you navigate complex financial matters, plan for your goals, and make wise investment decisions with your hard-earned money. But not all financial advisors are created equal. With so many options out there, how can you find an advisor who is truly qualified, has your best interests at heart, and will be a good fit for your needs?

There is a lot of debate in finance about the Efficient Market Hypothesis, and to what extent it applies to real markets. I’m generally an efficient markets proponent, but that’s not what this article is about. What I’d like to discuss is a lesser known side-effect of the Efficient Market Hypothesis that no one really talks about.

I often encounter questions about the best strategies for managing retirement savings. One common query is whether employees should transfer their 401(k) savings into an Individual Retirement Account (IRA) after retiring or switching jobs. The short answer is yes, and in this article, I will explain why this is generally a smart move for most people. I will also discuss the benefits of an IRA, the process of transferring your 401(k), and some potential pitfalls to avoid.

This post is very off-topic for me, but I just spent a lot of time trying to figure this out and figured I would make a post here in case it could help someone out in the future. Dig in!

Tax strategy is one of the three pillars of sound investment strategy, along with minimizing fees, and diversification. In this article, we will explore a wide range of tax-advantaged investment vehicles, including 401(k) and 403(b) plans, IRAs, SEP plans, HSAs, and 529 plans for children. We will also compare and contrast Roth and Traditional tax treatments and discuss advanced strategies such as tax loss harvesting, backdoor Roths, and more. Finally, we will delve into how tax considerations can inform portfolio allocation, including placing higher risk, higher return assets in tax-advantaged accounts and lower returning assets in taxable accounts.

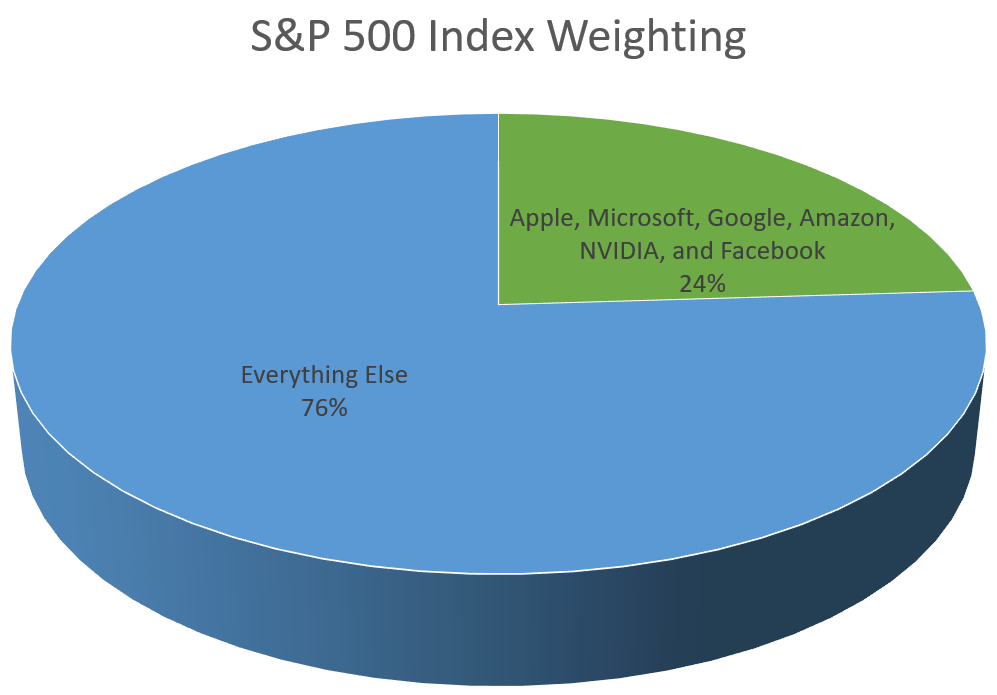

The S&P 500 index, a widely followed benchmark of the U.S. stock market, has long been considered a reliable indicator of the overall health of the economy. However, a closer look at the index reveals a surprising concentration in big tech stocks. This phenomenon is not only a reflection of the growing dominance of technology companies in the market, but also a result of the market-weighted structure of the index. Let’s explore the reasons behind this concentration and discuss the potential risks it poses to investors.